Blockchain technology and cryptocurrency have been powerful catalysts in generating wealth, but have also opened doors to starting new businesses far more efficiently than ever before. It can be a hassle getting a small business loan from a bank or pitching a business idea to investors and distracts from what’s important, doing what you love by building your business! The power from trustless and permissionless smart contracts and DeFi protocols removes friction imposed by banks (credit and background checks, predatory and sometimes prejudiced practices, etc) when raising capital for new businesses. This is truly DIY as you can leverage your assets to work for you instead of selling your crypto, dealing with taxes, and starting from scratch.

I’ve decided to share some anecdotes from my journey, as well as some revolutionary DeFi protocols that can help new business founders go around rather than jumping through hoops. I hope this helps new entrepreneurs utilize the power of Ethereum and Decentralized Finance protocols to avoid the time and costs of getting funding the traditional way.

First a few assumptions:

An entrepreneur has an “adequate” amount of crypto holdings on the Ethereum blockchain. This is very individual, and depends on the breadth of your business ambition.

The best forms of collateral in DeFi are ETH, WBTC, and stablecoins because they allow the highest amount of leverage (loan to value ratio) and are accepted across the majority of DeFi protocols

Small amount of startup capital to complete the following steps ahead of funding

Business plan (here’s an example from my MBA) to understand capital requirements/uses of funds

How much do you need to pay yourself?

Are you going to have to hire people or pay contractors?

Are there operational investments and expenses?

How long do you need to become profitable/break even (runway)?

Administrative steps to setting up your business:

Make a website - I used domain.com ($40) for hosting. It included basic webpage development tools for Ethropy.finance

Create a corporation (track costs)

S Corp or LLC - There are tax differences and advantages depending on the business needs. I am not an accountant or attorney so I can’t prescribe what’s best for your business, but I chose a S-Corp due to the tax advantages for payroll.

It’s helpful to complete all of the business incorporation forms using online legal assistance software - I used Zen Business ($463) and they helped me acquire:

State business license to allow you to conduct business in your local jurisdiction.

Federal Employer Identification Number (EIN) from the IRS.

Open a Business bank account - I used Chase, but this was only due to convenience. There may be local banks that have good options for small businesses (e.g. low/zero fees, savings accounts, point of sale integration)

You’ll be required to provide articles of incorporation and an EIN in order to set up with a bank.

Accounting - I’d recommend subscribing to some accounting software for tracking expenses, sales, receipts, payroll and taxes. This helps scale your business as it grows too.

I use Intuit quickbooks because it’s easy to use and affordable ($27/month)

Payroll and Benefits

Opolis - Opolis is an employment co-op, a startup created by the ETH Denver Hackathon founders. They take care of payroll, benefits, 401k, and can refer tax experts, very highly recommended! They have a deeply self-sovereign and crypto-centric ethos and are great guys to work with. No strings, no commitments, very helpful, and share the success of Opolis with members via their $WORK token.

Now that you’ve checked the administrative boxes, it’s time to fund the business. Let’s check out some excellent DeFi options, in order of my preference!

DeFi Funding Options

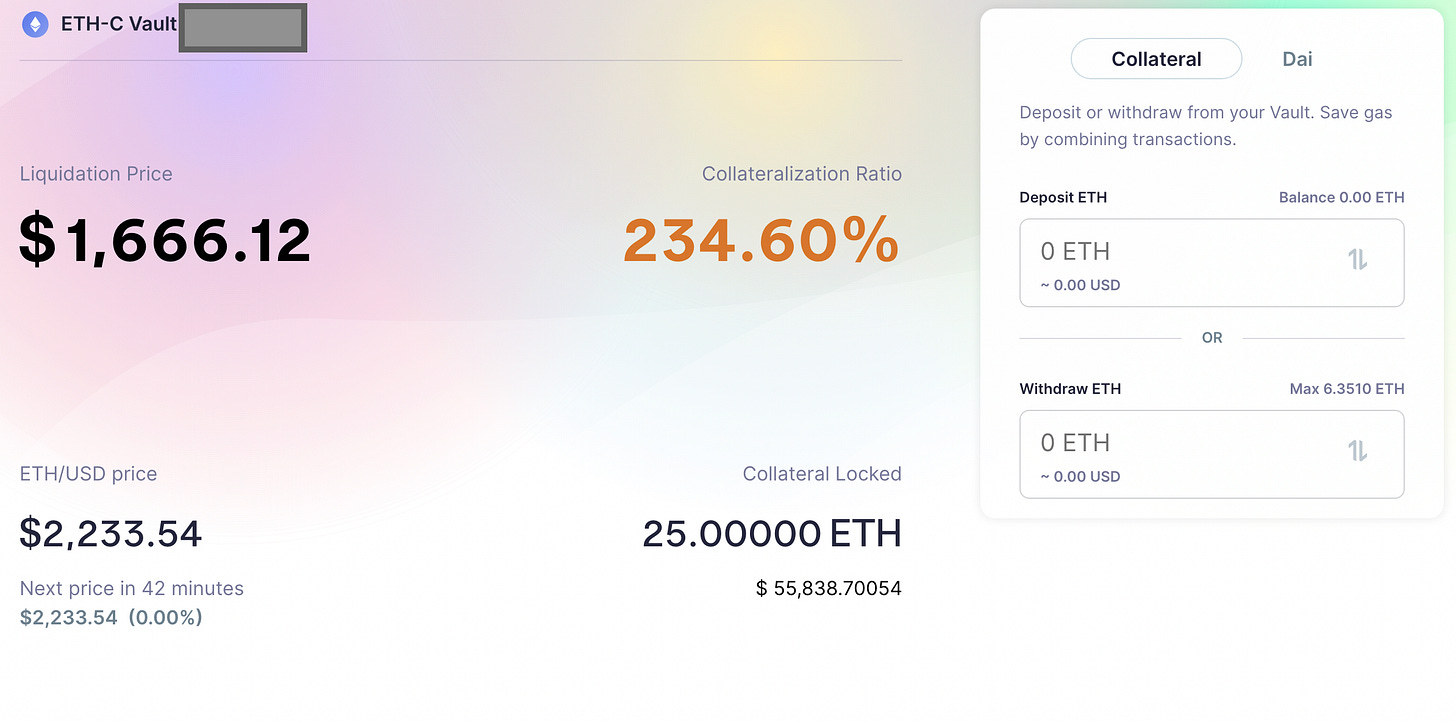

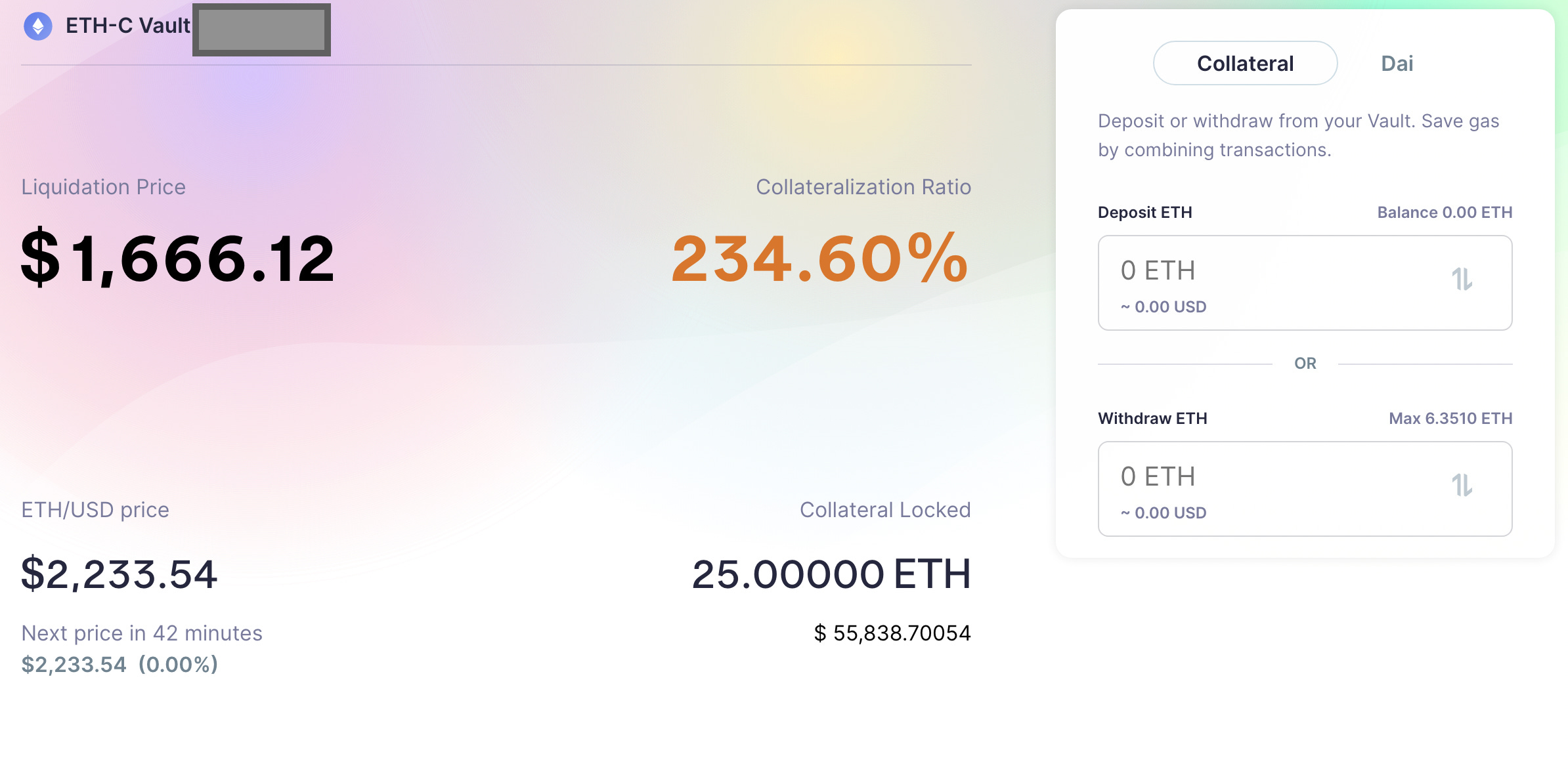

Option 1 - MakerDAO

Maker is the oldest DeFi bank and an OG protocol that allows depositors to mint a stablecoin called DAI. DAI is highly liquid and can be swapped for USD on most exchanges.

Depositors can select one of many types of collateral and create a crypto-backed loan. Each collateral has different collateralization ratio requirement, as more volatile assets need more collateral.

Interest rates depend on the type of collateral, the collateralization ratio, and protocol governance. Generally, interest rates are higher in bull markets because users are able to use DAI to invest in higher ROI opportunities.

Source oasis.app Risks

The interest rate should be factored into any business plan, and can change.

The volatility of the crypto market impacts a users’ vault collateralization ratio. When a bear market occurs, liquidations are possible and lead to instant selling of a depositors’ collateral + a 13% penalty.

Option 2 - Aave (Layer 1 or Polygon)

Aave is the most liquid crypto bank in DeFi. Aave also accepts multiple forms of collateral, and provides loans in multiple types of stablecoins, which provide depositors flexibility. Aave has deep liquidity on the Ethereum base layer, however, the expansion to Polygon has brought billions of capital and far cheaper transactions for funding.

Risks

Variable interest rates may appear low, but can surge as high as 50% or more in a liquidity crunch

Fixed interest rates are very high

Same as above, liquidation risk should be kept in mind

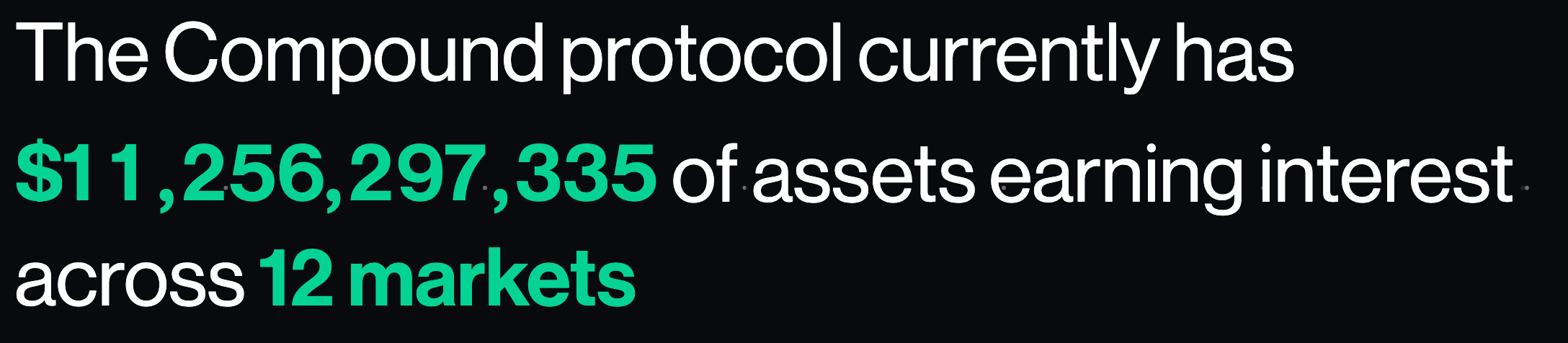

Option 3 - Compound Finance

Compound was the first crypto bank to incentivize deposits and loans with $COMP tokens. They were a major catalyst for last year’s DeFi Summer explosion on Ethereum.

Compound tends to have very reasonable interest rates, but have limited forms of collateral.

Risks

Same as Aave

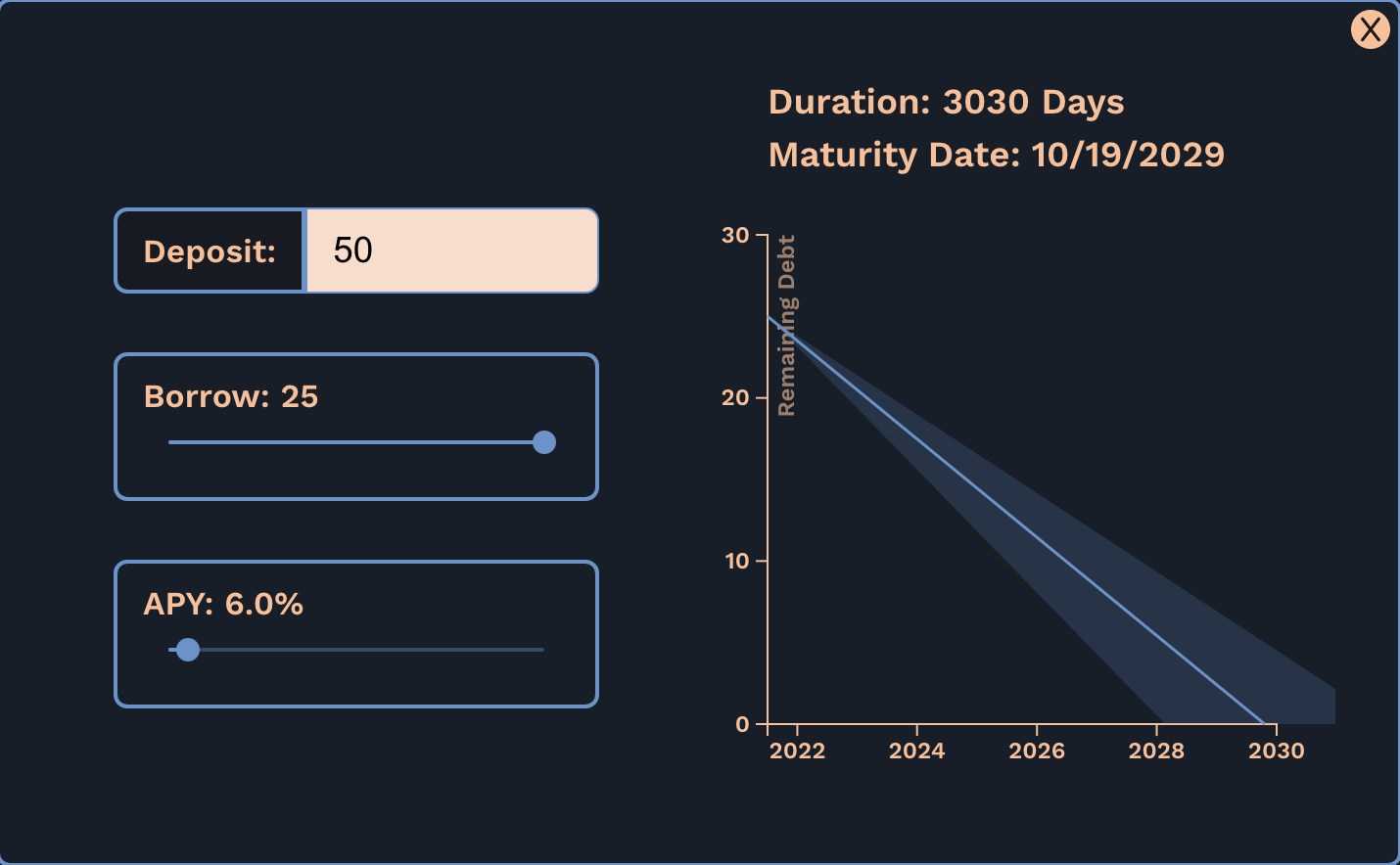

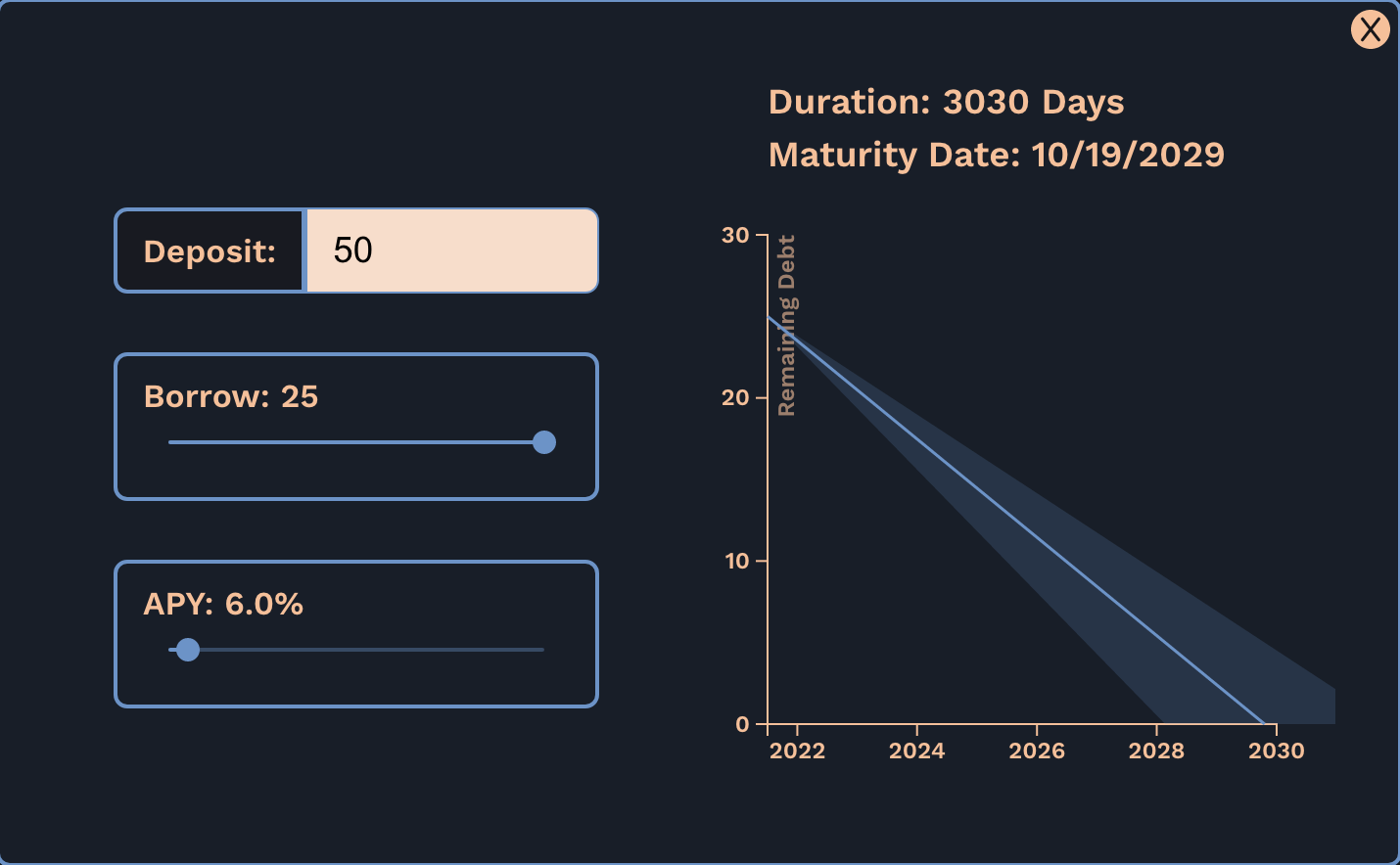

Option 4 - Alchemix Finance

Alchemix is a DeFi app that allows users to deposit DAI or ETH (WBTC and other stablecoins next) into the protocol and borrow up to 50% of the underlying collateral. This borrowed amount is future yield that’s generated by your original deposit using a yearn strategy.

alUSD loans can be swapped for DAI or USDC then for USD, and alETH loans can be swapped for ETH then sold to USD.

Payoff periods vary based on which collateral is deposited. These are between 5-10 years depending on the interest rate.

Source alchenix.fi ETH deposit and alETH loan If crypto prices increase, users can liquidate a portion of their collateral to pay off the debt faster.

Once the loan has paid itself back, users can withdraw their original deposit!

Risks

Payoff periods are variable as yields constantly fluctuate. During bear market periods, USD yields drop as crypto prices drop. During bull markets, yields increase making payoff periods shorter.

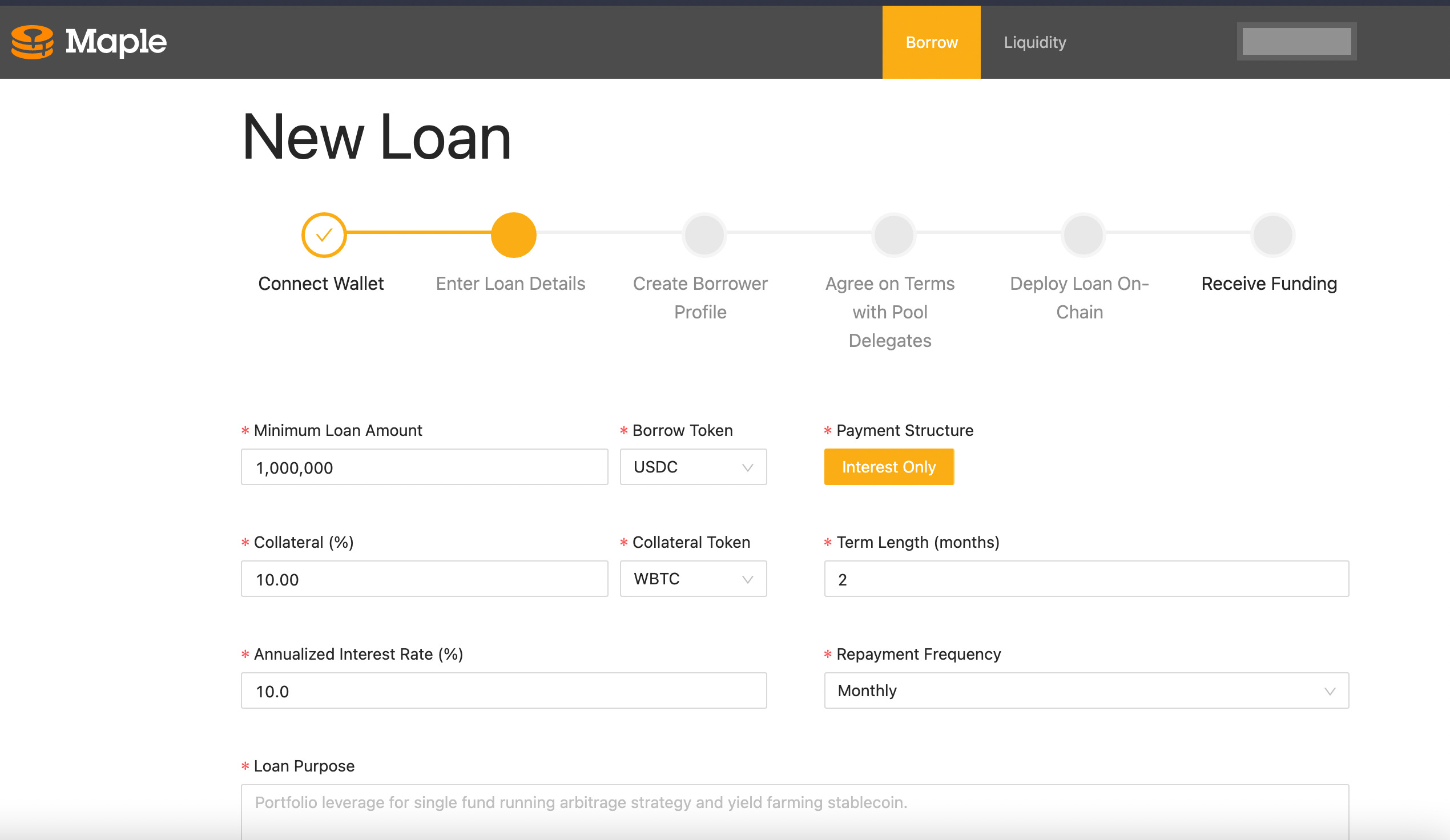

Option 5 - Maple Finance

Undercollateralized loans granted based on a user’s wallet history of borrowing.

Currently, only WBTC and USDC are accepted as forms of collateral

Users fill out a form stating their desired loan amount, length, collateral, interest rate, repayment frequency, and purpose

Risks:

New protocol with a lot of promise, but not much adoption

This may not be suitable for all users if cash flow isn’t being generated to pay down debt regularly

Option 6 - Gitcoin grants or DAO grants/investments

Gitcoin has helped many teams fund ideas. It’s a brilliant protocol that applies quadratic funding/matching to donations for projects. Anyone is able to set up a Gitcoin grant page for their idea!

Many DeFi protocols are now funding new projects with their rich and growing treasuries. Aave, Uniswap, Sushiswap and others like Stacker Ventures are providing capital to entrepreneurs with ideas that can help the ecosystem or protocol growth. This is a bit more permissioned, but can be a superior experience than convincing the old guard (a bank) to fund your business.